In the second half of 2022, GDP in Israel grew by 6.8%. Despite controversies regarding Palestine, Israel has more startups per capita, approximately one for every 2,000 Israelis, and is a key state in the technology sector.

Israel is one of the most controversial states in the world. It is currently recognised internationally by 164 of the 192 member states of the United Nations. Israel is mostly known for its religious and territorial confrontation. Since its foundation, this state has been immersed for decades in a host of internal and external political conflicts and wars; standing out with the Arab states over the Palestinian question. One fact to note, the Arab League has established a boycott of Israeli companies and products made in Israel, since the founding of this state.

Another side of this state that is becoming more widely known, Israel is a pioneer in the field of technology. The country has more than 4,000 technology companies, of which 500 generate annual revenues of more than $20 billion. In turn, 80 of the 500 largest companies in the world have subsidiaries dedicated mainly to R&D in the country, which places Tel Aviv, after Silicon Valley, as the world's leading area in technological investment and innovation, and almost 50% of its exports come from the high-tech sector.

Israel allocates 4.3 percent of GDP to R&D, more than Finland (3.9 percent) or South Korea (3.6 percent). This turnaround is noteworthy after the severe economic crisis during the 1980s. The following article will set aside the controversy and shed light on the keys to Israel's economic success.

Modern Israel began in the 1880s. From 1881-1903, the first wave of Jewish population immigration, known as "aliyah", took place. The second aliyah is noteworthy. Between 1904-1914, the second great immigration wave of Jews took place, about 40,000. They mainly came from Eastern Europe, but also from other territories such as Yemen. It should be noted that during this time it was made up of socialist Jews.

These socialist pioneers started the kibbutz movement. Kibbutz have been collective farms to overcome the adversities of climate and territory, while laying the foundation for a new national home where they would not be persecuted. They also functioned as a network of mutual support and security for newly arrived immigrants.

In 1880, the total number of Jews in this region was 20,000 to 25,000, two-thirds of whom were located in Jerusalem. It is important to note that not all the inhabitants of the area rejected the arrival of Jewish immigration.

The first kibbutz, called Degania, was founded in 1910, and the great majority of them were founded between 1930 and 1940, years before the creation and foundation of the current state of Israel. During World War I, the United Kingdom and France held a conference to divide the Middle East, materialized in the Sykes-Picot Agreement. In 1917, under the command of the British General Allenby, defeated the Ottoman army and, at the end of that year, supported the creation of "a Jewish national home", embodied in the Balfour Declaration.

Image 1: Members of a kibbutz in 1937. Source: https://www.britannica.com/topic/kibbutz

With the successive arrivals of aliyahs, new infrastructures for food trade and water canalization were created, as well as the introduction of new techniques in the fields and new crops, and the kibbutz were modernised and militarized. In 1920, the paramilitary organization, known as "hagana", the forerunner of today's Israeli army, was created. During these years, the first universities were established: the Technion and the Hebrew University of Jerusalem, in 1912 and 1918 respectively.

After World War II and the horror of the Holocaust, Resolution 181 of the UN General Assembly proposed the creation of an Arab and a Jewish state and an international zone in the cities of Jerusalem and Bethlehem. The Jews accepted this proposal, but not the Arabs. In 1948, the day after the proclamation of the State of Israel by David Ben Gurion, Egypt, Syria, Transjordan (now Jordan), Lebanon and Iraq declared war on this new state and tried to invade it without success.

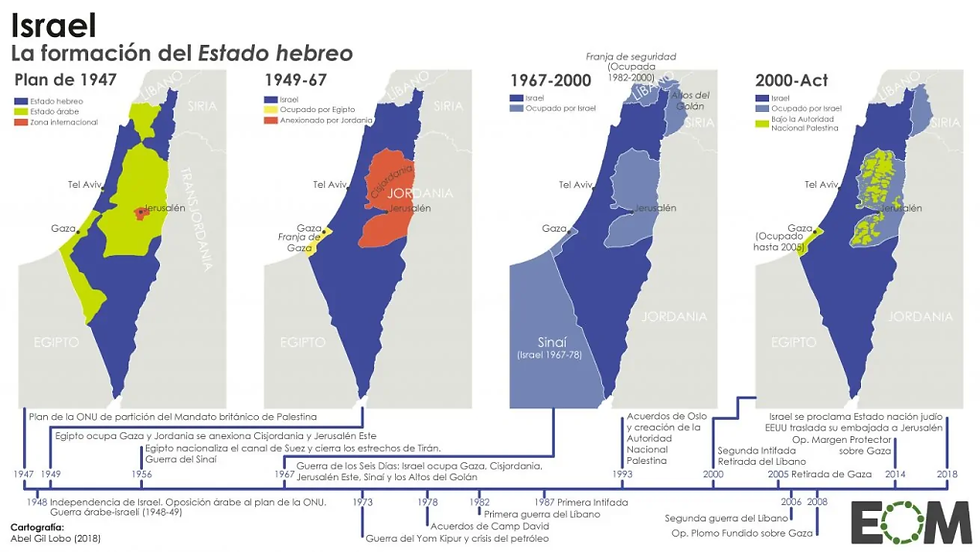

Map 1: formation and evolution of Israel. Source: https://elordenmundial.com/egipto-e-israel-de-enemigos-mortales-a-aliados-fieles/

During the 1950s and 1960s, the impact of immigration forced the rationing of resources such as oil and food, with the government deeply involved in the economy. From 1950 to 1955, the Israeli economy grew about 13% each year, and just under 10% in the following years until the 1960s. The government provided jobs and launched infrastructure projects using money from abroad.

From the 1960' s onwards, the kibbutz expanded in both quality of life and population, but the Israeli economy was based on agriculture. Israel suffered a wrenching economic crisis in the early 1980s whose roots were rooted in the 1973 Yom Kippur War and the ensuing oil embargo that lasted until 1985. This period known as the "lost decade," Israel's economy witnessed near zero per capita growth, hyperinflation (in 1984 it was 445%) and galloping deficit and debt levels. During this time, both the business and quasi-government sectors (health insurance, pension plans, kibbutzim) became completely inefficient and almost totally dependent on the government, which at the time accounted for 70% of GDP.

In 1985, the tables were turned with the implementation of the Stabilisation Program. A total price freeze was imposed on all goods and services and the peg mechanism was suspended. This plan succeeded in curbing inflation from 400% to 20%, stabilized the balance of payments and, above all, reduced the deficit from 15% of GDP to a surplus of 1%. By 1986, public spending had been cut and the government was legally prohibited from printing money to cover the deficit. The massive reduction in spending forced the private and quasi-public sectors to become more efficient, as government financing could no longer be relied upon.

Between 1985 and 1990, the private sector made great strides in efficiency and worker productivity, while unions were weakened and management was given the ability to fire employees at its discretion. However, Israel did not have as advanced a financial and technological sector as it does today. The situation would change during the 1990s, with another aliyah of Jewish population from the former USSR. Between 1990 and 1991, some 400,000 would arrive.

To this end, in 1991, the Israeli government made an important strategic decision. It gradually opened the consumer goods, currency and investment sectors to international competition. In addition, customs duties were slowly reduced to the point where effective tariff protection is now less than 1%.

In addition, in 1991, some 24 incubators were developed for the development of innovative technological products. At the same time, the Inbal Program was created. This plan was an insurance scheme that tried to stimulate the creation of venture capital funds, although the program failed due to the lack of liquidity of the assets. Despite this first failure, in 1992, the Yozma Program (yozma-initiative) was launched.

The Israeli government earmarked US$100 million to develop the start-up and venture capital system. To spearhead the investment, it created The Yozma Group, a body responsible for developing the country's venture capital industry. This plan had a clear objective: to create a start-up and venture capital industry.

The Yozma did not intervene in the management and offered its international private partners the opportunity to buy back their stake at cost plus interest. The results were immediate: In just 2 years, the Israeli government, by investing $100 million, managed to create 10 venture capital funds, with an overall investment capacity of $263 million.

Most of the money that fueled Israel's technological rise came from the Israeli government or U.S. technology companies. The bursting of the high-tech bubble and, the Second Intifada (2000-2005), impacted the Israeli economy and society. There was a drop in tourism, foreign investment and local consumption.

This escalation of tensions occurred during the government of Ariel Sharon, with Benjamin Netanyahu (known as Bibi) as Finance Minister (2003-2005). Netanyahu cut social spending in education, health care and the safety net. At the same time, he reduced the weight of the state, cut the state budget, privatized government functions, and reduced taxes, for example, the corporate tax went from 36% in 2003 to 25% in 2010.

Image 2: left: Benyamin Netanyahu with former Israeli Prime Minister Ariel Sharon in 2003. Source: https://www.timesofisrael.com/israels-political-leaders-mourn-great-warrior-extraordinary-leader/

This first plan had an immediate result. Between the last half of 2003 and 2008, the Israeli economy grew at an average annual rate of close to 5% and the size of the public debt was reduced from over 100% of GDP in 2002 to 80% in 2008. In 2009, Netanyahu was elected as Prime Minister of Israel and adopted the same economic policy in a state with a strong socialist influence on the economy.

Netanyahu initiated a culture of continuous reforms to develop an environment in which private sector players could thrive, in order to curb excessive bureaucracy and regulations. In 2009, he reduced the size of the public sector, controlled government spending, cut tax rates and streamlined the tax system, privatized major state-owned industries such as banks, oil refineries, the national airline and Zim Integrated Shipping Services, reformed the pension system, among other reforms.

Since the first commercial discovery of natural gas in 2000, Israel's energy situation would change dramatically. 2009, however, would be a key date. In 2009, the US company Noble Energy and its local partners discovered the Tamar field and, in 2011, the Leviathan field. This has made Israel a net exporter and would open new diplomatic doors, especially with other Arab states.

At the end of 2013, the Israeli parliament, The Knesset, passed the Promotion of Competition and Reduction of Concentration Law, to increase competitiveness in the Israeli economy. In the same year, Netanyahu also initiated a port privatization campaign to increase Israel's exports. In July 2013, he issued tenders for the construction of private ports in Haifa and Ashdod.

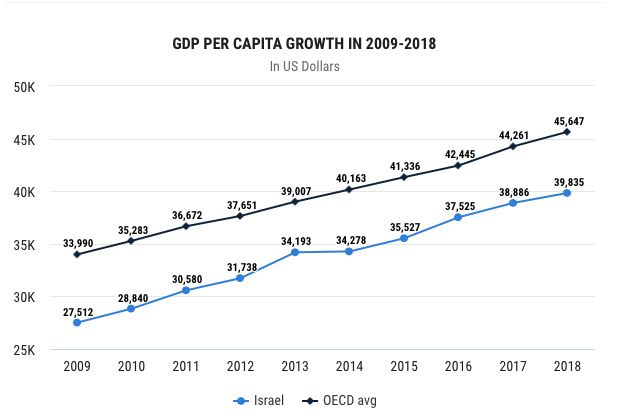

During these years, Israel would undergo a change and cement its global and strategic position in the high-tech sector and in the areas of: digital health, smart mobility, agrotechnology, water and cybernetics. Other facts about this economic transformation are as follow. Per capita GDP grew by 60% between then and 2020, from $27,500 to $43,689, and now ranks Israel among the top 20 nations in the world, while unemployment reached an all-time low of 3.4% in the months before the SARS-CoV-2 crisis.

Figure 1: GDP per capita growth (U.S. dollars) in 2009-2018. Source: https://www.timesofisrael.com/is-netanyahu-an-economic-wizard-the-numbers-beg-to-differ/

In 2016 and 2018, respectively, Israel signed two agreements with Jordan and Egypt to export natural gas to these two states. In addition, in 2020, Cyprus President Nicos Anastasiades, Greek Prime Minister Kyriakos Mitsotakis and former Israeli Prime Minister Benjamin Netanyahu signed an agreement for the construction of the East-Med. The East-Med is a gas pipeline under construction that will connect Israel's gas reserves with Greece, destined for other southeastern EU states.

In the same year, due to the economic and health crisis resulting from SARS-CoV-2, in March 2020 the unemployment rate exceeded 20%. According to a Pew Research Center survey, the majority of Israeli citizens think that the country has effectively handled the coronavirus outbreak.

At the same time, the Abraham Accords were signed. Under the Abraham Accords, Israel, the United Arab Emirates and Bahrain normalised and publicly formalized their diplomatic ties. They also became a term to describe the other normalisation agreements that Israel signed after the initial declaration, with Sudan and Morocco.

However, in April 2021 after a harsh confinement, unemployment fell to less than 9.5%. Despite Israeli political instability, in December 2021, the OECD stated that the Israeli economy was rebounding strongly in 2021, beating forecasts, and in 2021, it grew by 7%. Israeli exports will reach a record $135 billion to $140 billion in 2021, up 18.5% from last year. The majority of Israeli exports (excluding diamonds) went to the European Union (39%), followed by the United States (33%) and Asia (25%).

Currently (July 2022 data), the current inflation rate in Israel is 5.21% (excluding food and energy prices). According to a study by the Money.co.uk website, housing prices in Israel increased by 345.7% in the last decade. Another key factor will be the labor participation rate, especially of the haredi community and the Arab population. In addition, rising food prices, falling wages and energy prices will determine the outcome of the elections to be held in November 2022, and the fragile political stability. However, Israel has been able to cope with the problems in order to regain its economic position and technological leadership.

Recommended bibliography:

Ben-David, R., 2022. Cost of living, economy are top priority for voters in upcoming election — survey. [online] Timesofisrael.com. Available at: https://www.timesofisrael.com/cost-of-living-economy-are-top-priority-for-voters-in-upcoming-election-survey/

Salomon, S., 2018. From 1950s rationing to modern high-tech boom: Israel’s economic success story. [online] Timesofisrael.com. Available at: https://www.timesofisrael.com/from-1950s-rationing-to-21st-century-high-tech-boom-an-economic-success-story/

Comments